MDI Mortgage Lending Snapshot

- Elise Pietro

- May 27

- 4 min read

It’s been a tumultuous time for the U.S. housing market. COVID-19 and widespread remote work transformed housing preferences overnight, with people moving out of urban cores and demanding more space. Low interest rates spurred record numbers of home purchases and refinances. Then came the slump as interest rates rose, housing supply remained low, and new headwinds in construction and labor costs materialized. i

In this snapshot of mortgage lending by minority depository institutions (MDIs), we take stock as the market began to normalize. We use the most recent available data, from 2024.

Figure 1: MDI Mortgage Lending Activity

Figure 2: MDI Originated Loan Characteristics

Of almost 56,000 reported loans, 62% were originations (see Figure 1).ii These originations were largely bread-and-butter transactions – people purchasing a single-family home they intended to live in (see Figure 2). Most originations were conventional, meaning borrowers qualified without government support, and almost half were sold on the secondary market. This frees up bank balance sheets, allowing MDIs to keep capital revolving in the local economy.

For the rest of our analysis, we look at only bread-and-butter mortgage originations: single-family homes purchased as a primary residence using a closed-end, forward mortgage.

In total, 25 MDIs originated 20,450 loans worth over $7.4 billion in 2024. While the median MDI originated about 240 loans, the top five lenders averaged over 3,000 loans each and together accounted for 75% of the total loans made.

This concentration reflects the advantages of specialization and scale for a small number of lenders, even as many community banks have exited mortgage financing. For example Gateway First Bank, which originated over a third of the MDI sector’s loans, was an independent mortgage lender that only entered retail banking after a 2019 acquisition. In Puerto Rico, MDIs controlled 38% of the island’s mortgage market. These are not widely replicable strategies for the community banking sector, including the many MDIs that have struggled to maintain a durable mortgage financing business.

As Figure 3 shows below, MDIs were active in every state except North Dakota. Almost 70% of mortgages went to Puerto Rico and five states – Massachusetts, Texas, Oklahoma, New York, and California. Not incidentally, this is the established footprint of the top lenders.

Figure 3: MDI Mortgage Lending by County

Looking at mortgage lending by MDI type (see Figure 4), Asian MDIs originated 37% of loans but 56% of total loan dollars, meaning that the financing is going towards relatively expensive houses. Hispanic MDIs, in comparison, are financing cheaper homes primarily in Puerto Rico.

Figure 4: Mortgage Lending by MDI Type

The Native MDI sector, led by Gateway First Bank, originated a much larger share of both loans (37%) and loan dollars (25%) than its share of MDI lenders (16%) would suggest. Black MDIs, meanwhile, originated just 325 mortgages – or 2% of the MDI sector’s loans.

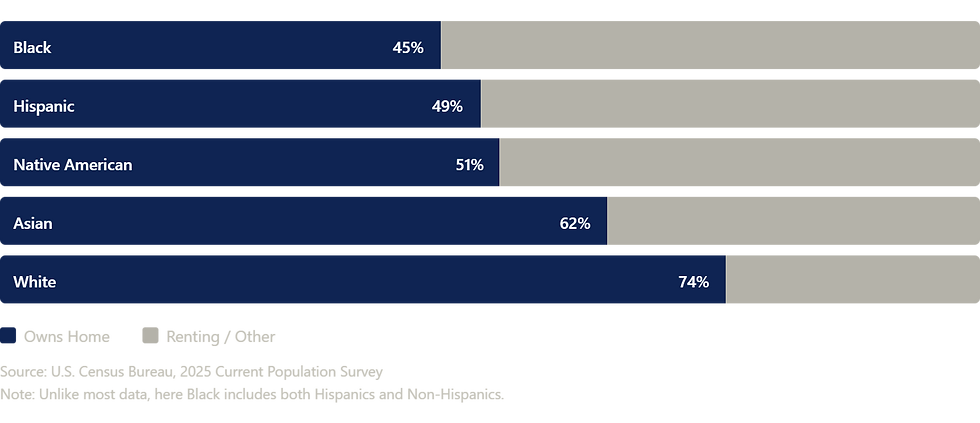

Our previous research outlined the difficulties MDIs face in mortgage financing, but this lending remains critical. Homeownership is key to building wealth, and the gaps in who owns their home have been large, persistent, and consequential over time (see Figure 5).

Figure 5: Homeownership Rates by Race/Ethnicity

Home equity is 45% of the median household’s wealth, but for the median Black and Hispanic households it is 63% and 66%, respectively. In other words, without access to homeownership, a large portion of people’s wealth is erased. These gaps compound across generations, as less wealth means people are less able to fund a business, pay for college, or otherwise secure their children’s future.

Policymakers are increasingly focused on making homeownership more accessible. Local officials are updating zoning laws and exploring new public-private partnerships. Congress is considering legislation that incentivizes construction through an all-of-government approach at the federal level.

On the financing side, banks largely exited the home mortgage market after the 2008 Financial Crisis, as changes intended to prevent another recession proved overly restrictive for community banks. Regulators are now rebalancing, trying to help banks better compete with independent mortgage companies. Because while non-bank lenders offer speed and scale, they are less adept at working with the financially underserved and are not typically embedded in local communities.

In comparison, our previous research finds that MDIs originate a higher share of mortgages to low-income borrowers, have lower denial rates, and assist borrowers who often have lower credit scores or smaller down payments. MDIs are also proven at closing homeownership gaps: for example, compared to all U.S. mortgage lenders, Chickasaw Community Bank had the second highest lending rate to Native American home buyers.

MDIs are exactly the type of mission-driven, local community banks that housing affordability plans need to prioritize.

At the National Bankers Association, we work closely with our member banks to invest in technology and partnerships, reduce compliance burdens, and advocate for needed policy updates. And through our current housing initiative, we are helping MDIs scale their mortgage operations to meet the vital needs of the communities they serve. We invite you to learn more and join us in this important work.

Acknowledgements

Our thanks to former intern Wajeeha Amir for her research assistance. Thank you also to the Kresge Foundation, whose funding supports both this blog and our broader Foundation housing initiatives.

[1] See for example Sami Sparber. (2025). “How the Pandemic Transformed the Housing Market in 5 Years.” Axios.

2 Financial institutions are required to publicly report under the Home Mortgage Disclosure Act (HMDA) if the institution had $55+ million in assets and 100+ closed-end originations (or 200+ open-end originations) in each of the previous two years. Under HMDA, financial institutions report loans or applications when one of the following actions is taken: loan originated, application approved but not accepted, application denied, application withdrawn by applicant, file closed for incompleteness, loan purchased, preapproval request denied, and preapproval request approved but not accepted.

Comments