How MDIs Can Expand Access in America's Banking Deserts

- Elise Pietro

- May 6

- 3 min read

At the National Bankers Association, we know that banking matters: it gives people a safe place to store their money, provides opportunities to invest and build wealth, and facilitates capital circulation in the local economy.

The association is also committed to expanding access to the essential services that banks provide to their communities. This is now easier, thanks to recently published data on banking deserts. The new Federal Reserve dashboard identifies neighborhoods without any bank branches (banking deserts) or only one branch (potential deserts), which combined we refer to as low banking access areas.[1]

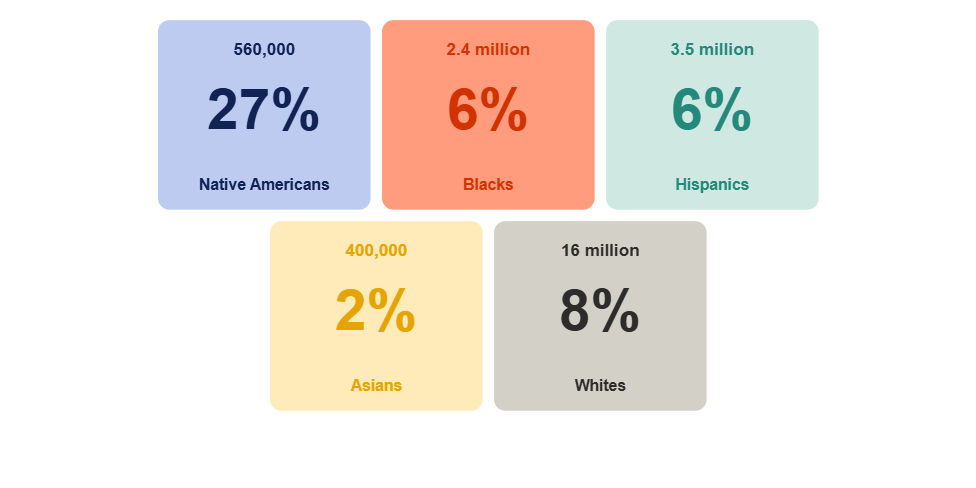

In 2025, 4% of census tracts were banking deserts and another 4% were potential deserts, meaning 23.5 million people had limited or no access to a bank in their neighborhood. Nationally, 7% of Americans have low banking access, but there is variation across racial and ethnic groups (see Figure 1). [2] One critical concern: over a quarter of Native Americans live in low banking access areas.

Figure 1: Low Banking Access by the Numbers

Most banking deserts or potential deserts are majority White (78%), but 66% of Native American-majority neighborhoods have low banking access (see Figure 2). In other words, only 3% of banking deserts or potential deserts are majority Native American, but if you live in a Native American-majority neighborhood there is a 2 in 3 chance that you are in a low banking access area. Structural barriers like this ultimately feed into gaps in financial wellbeing.

Figure 2: Low Banking Access in Majority-Minority Census Tracts

These days it’s possible to complete most banking transactions without ever stepping foot inside a physical branch – almost 70% of households rely primarily on online or mobile app options. Digital banking is not a silver bullet, however.

People who are older, lower income, less educated, or live in non-urban areas – those already financially underserved – use in-person banking more frequently. When applying for loans or making other big financial decisions, many people prefer a personalized, face-to-face discussion.

However, low banking access areas that are majority-minority, when compared to majority White areas, are more likely to have low broadband access (1.7 times) and computer usage (1.6 times). This leaves people in a tough spot. Their nearest bank branch is on average 10 miles away, but for some it can be dozens or even hundreds of miles.

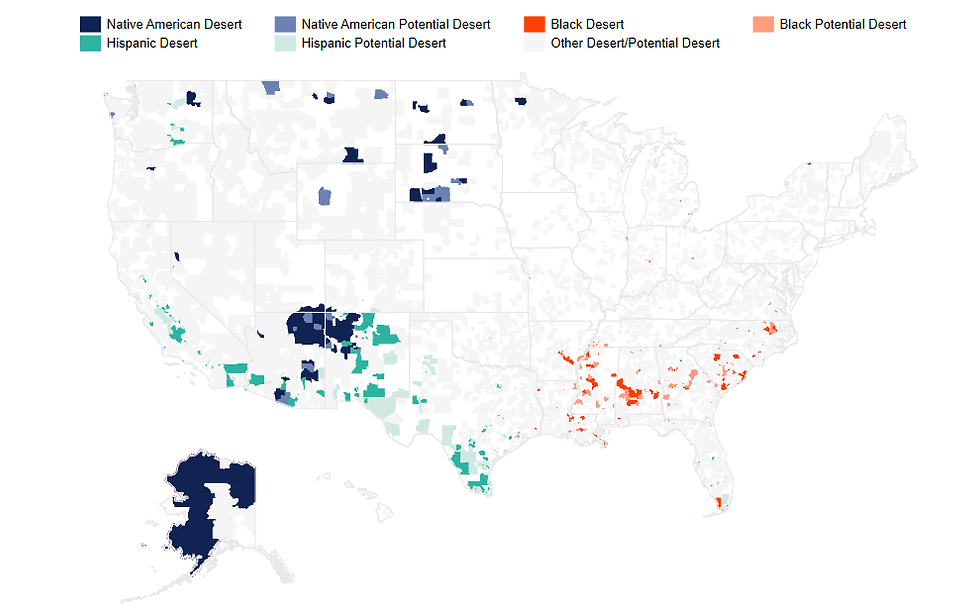

Figure 3: Banking Deserts and Potential Deserts, by Racial/Ethnic Majority

Banking deserts exist across the country, as Figure 3 shows. Persistently underserved regions include Tribal lands in Alaska, the Southwest, Montana, and Plains states; Hispanic agricultural communities in California’s Central Valley, New Mexico, south Texas, and Washington; and Black Belt neighborhoods across the Southeast.

This is not new. Minority communities have fought disinvestment for generations, not least by creating their own banks. The landmark 1977 Community Reinvestment Act was an attempt to mandate financial institutions provide services in all areas where they take deposits, including historically underserved communities. Yet almost 50 years later, too many people are still poorly served by the banking sector.

Mission-driven community banks – and Minority Depository Institutions (MDIs) in particular – are ideal candidates to reach these low banking access areas.

There are a number of avenues to pursue. As financial services merger and acquisition activity picks up, strategic MDIs should look for opportunities to expand their footprint in these low banking access areas. Key regulators are focused on supporting de novo banks. The Community Development Financial Institutions (CDFI) Fund provides low-cost funding for banks and similar entities working in underserved areas. Native CDFIs have been especially critical in closing financing gaps in Indian Country.

We encourage everyone to think creatively about how they can help expand opportunity to all Americans. To learn more about the work we are doing at the National Bankers Association or to partner with us, please visit our website.

[1] In the Federal Reserve dataset, bank branches are defined as brick and mortar, non-in-store, full service, and retail branches. Banks and credit unions are included, but not non-bank or non-credit union CDFIs.

[2] Racial categories are defined by the U.S. Census Bureau and are mutually exclusive. Figure 1 omits 630,000 people who live in low banking access areas and self-categorize their race as 2+ Races or Other.

Great read on how MDIs can fill banking deserts and help communities thrive. It reminds me how useful tools like Free Analog Clock Online can support learning, whether it's about money or telling time, for kids and adults alike.

Expanding opportunities should always be a priority. The same principle applies across many areas, from financial inclusion to community-driven platforms like skribbl io that encourage participation.

시간을 효율적으로 활용할 수 있는 서비스를 찾던 중 좋은 선택을 하게 되어 만족스러웠습니다. 처음 문의할 때부터 친절한 응대를 받을 수 있었고 진행 과정도 매우 깔끔했습니다. 이용 중에는 상품권매입 서비스가 신속하게 처리되어 기다림이 거의 없었으며 필요한 안내도 자세하게 제공되었습니다. 전반적으로 믿음이 가는 서비스였고 앞으로도 계속 이용하고 싶은 생각이 들었습니다.

Thanks for highlighting this important issue. Equal access to financial services is essential for stronger communities. I enjoy fnaf in my free time, and I also appreciate articles that raise awareness about real-world challenges and solutions.

평소 생활비를 조금이라도 아끼고 싶어 이용해 봤는데 기대 이상으로 편리했습니다. 결제 전 비교해 보니 혜택이 있어 부담을 줄일 수 있었고 사용 방법도 쉬워 누구나 편하게 컬쳐랜드할인 활용할 수 있겠다고 느꼈습니다.