Addressing The Capital Gap: What the 2026 Small Business Credit Survey Reveals About Minority Entrepreneurs

- Anthony Barr

- Mar 26

- 4 min read

Every year, the Federal Reserve's Small Business Credit Survey (SBCS) captures the financial pulse of America's small businesses. The 2026 edition delivers an urgent message: minority-owned employer firms are operating under significant financial strain and are struggling to access capital. For Minority Depository Institutions (MDIs), Community Development Financial Institutions (CDFIs), and other mission-driven lenders, these findings underscore a significant opportunity to help strengthen small businesses.

Finding 1: Minority-Owned Firms Are Financially Vulnerable

The 2026 SBCS reveals significant financial vulnerability among small businesses. When asked to describe their firm's financial condition, only 51% of white-owned firms reported a "Poor" or "Fair" condition, versus financially thriving. Yet overwhelming majorities (67% to 77%) of minority-owned firms rated their condition as "Poor" or "Fair."

Profitability tells the same story of financial strain. Most firms continue to report higher input costs which are compressing margins. And for the second consecutive SBCS survey, firms were more likely to report that revenue decreased in the last 12 months than that it increased (see last year’s survey here.) Higher costs and lower revenue means that many firms are currently operating at a loss, including 58% of Native-owned firms, 47% of Black-owned firms, 41% of Hispanic-owned firms, 38% of Asian-owned firms, and 32% of White-owned firms.

Some of the profitability disparities are structural. For example, a higher percentage of surveyed minority firms are 0-2 years old and a higher percentage are concentrated in the lowest revenue tiers where there are fewer economies of scale. But the survey points to other potential challenges for minority firms including 1): struggles reaching new customers and increasing sales; 2): lower likelihood of raising prices to offset costs which suggests weaker pricing power relative to other firms; 3): and lagging technology adoption and utilization.

Yet despite these headwinds, entrepreneurs remain remarkably optimistic. Most surveyed firms from almost all racial groups expect revenue growth over the next 12 months including for Black (74%), Hispanic (64%), Native (61%), and White-owned firms (57%.)

Many of these small business owners have ambition to grow. But too often, these entrepreneurs lack the access to capital they need to fuel that growth.

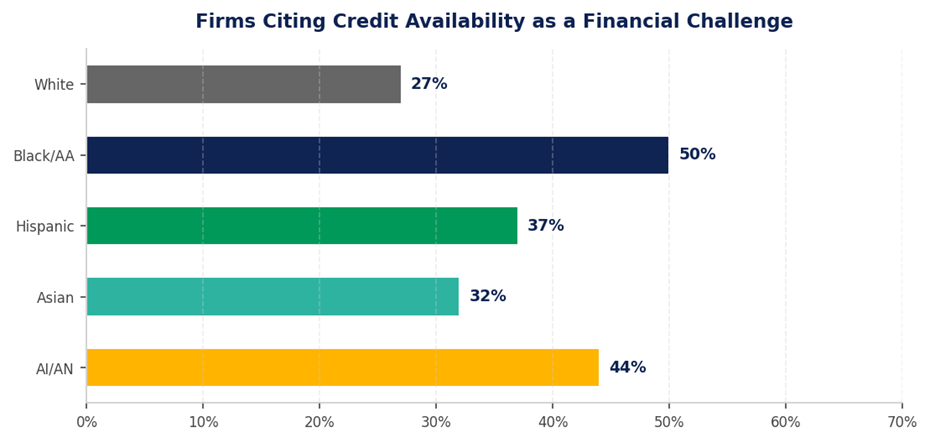

Finding 2: Credit Access Is A Defining Challenge

When minority business owners describe their financial challenges, credit availability is a recurring issue in a way that it isn’t for White-owned firms (see fig. below).

Notably, minority firms are also more likely to seek credit to cover operating expenses, rather than to create a savings buffer or to expand the business. This underscores the financial vulnerability that these firms face.

Finding 3: Mainstream Lenders Are Not Closing Credit Gaps

Minority business owners are applying for credit at high rates but often do not receive the credit they need. For example, at large banks, only 16% of Black applicants received the full amount they sought, compared to 48% of White applicants. And nearly half (48%) of Black applicants at large banks received nothing at all.

When denied, 55% of Black-owned firms cited a low credit score as the reason — the top factor, above collateral, debt levels, or weak sales. Low credit scores was also a major reason for denials among Hispanic (42%) and Asian (31%) firms. This highlights the need for alternative scoring and underwriting frameworks (such as based on cash-flow) that mission-driven lenders can use to safely provide more capital to businesses in need.

Finding 4: Discouragement Is Stifling Demand Before It Starts

Perhaps the most alarming finding is the entrepreneurs who need capital but have been conditioned by past rejections and experiences of perceived bias to believe the system will not work for them. Among firms that chose not to apply for financing, 32% of Black-owned businesses cited discouragement as their primary reason — four times the 8% rate among White-owned firms. Hispanic-owned firms reported a 21% discouragement rate.

Discouraged borrowers represent a significant, underserved market. Minority banks that invest in community outreach and trust-based relationships can reach this population that mainstream lenders will never see.

Conclusion: The Opportunity Is Now

The 2026 SBCS survey underscores urgency: without intervention, many firms will become trapped in a reinforcing cycle: young firms + thin revenues + weak customer reach → revenue declines → operating losses → high credit risk → no affordable capital to bridge the gap → continued losses.

For MDIs and other mission-driven lenders, this urgency also reflects a significant opportunity. By leveraging relationship-based lending along with cashflow underwriting, these lenders can convert a documented market failure into deposits, loans, and lasting community wealth.

The National Bankers Association Foundation is proud to support MDIs as they serve small businesses. In partnership with the DC Community Development Consortium (DCCDC), our new BOSSTANK initiative is providing back-office support to small businesses in DC’s Wards 7 & 8 with a goal of strengthening these firms and improving their ability to access capital. We plan to expand this initiative to more geographies soon.

To learn more about how you can partner with the National Bankers Association Foundation around small business and across our other pillars, click here.

This blog is based on analysis of the 2026 Federal Reserve Small Business Credit Survey. You can access the full dataset here: https://www.fedsmallbusiness.org/reports/survey/2026/2026-report-on-employer-firms

I enjoy how Drive Mad focuses on balance rather than speed alone. Reaching the finish line often depends on understanding the terrain instead of rushing forward.

Watching a character evolve from an ordinary child into a successful individual offers a unique sense of satisfaction. This is the factor that enables BitLife to foster a lasting connection with its global player community.

É muito legal ver comentários e dicas sendo compartilhados de forma tão simples aqui. Ultimamente, tenho praticado um teste de reflexos para melhorar minha agilidade, precisão e habilidades com o mouse.

Combined with energetic sound effects, it creates an immersive environment that keeps players hooked. Overall, Slope Rider 3D is a perfect choice for anyone looking for a fun, fast, and challenging game to enjoy in short bursts or longer sessions.

This piece really highlights a tough reality that often goes unseen. The cycle of limited access to capital and financial vulnerability feels frustratingly persistent. What stood out to me most is the level of optimism entrepreneurs still carry despite these barriers. It reminds me of how even in something simple like basketballlegends, a game, you keep pushing forward no matter the odds. That same resilience clearly exists here.